In M&A transactions, the effectiveness of due diligence is often mistakenly assessed by the breadth of review or the volume of issues identified. In practice, transactions rarely fail due to a lack of information. Rather, they fail because transaction-critical risks are either not identified, or not properly assessed and addressed.

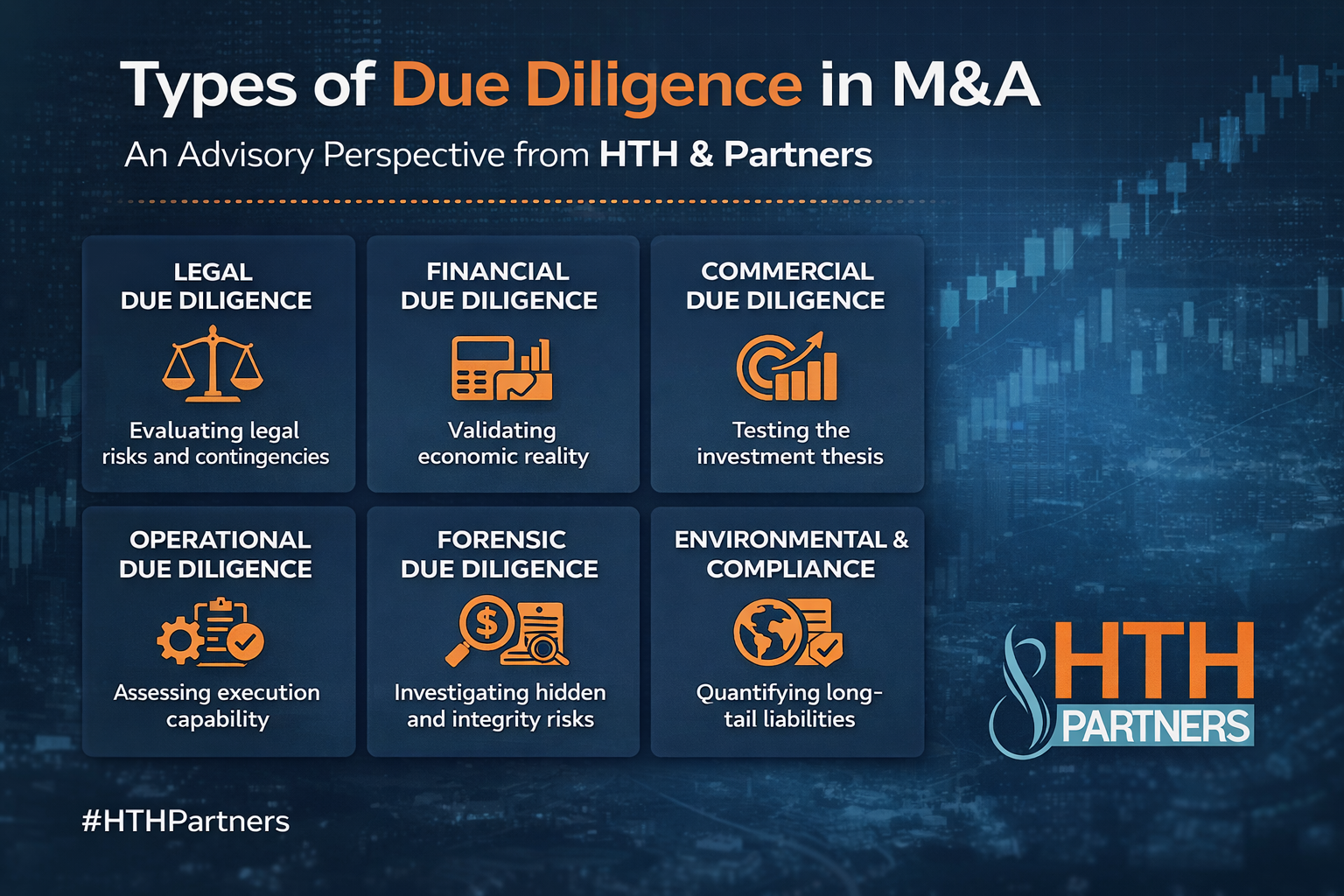

From an advisory perspective, legal due diligence should not be viewed as a compliance exercise or a procedural review. It is a structured analytical process designed to identify risks that may affect transaction value, execution certainty, and post-closing outcomes. Within this framework, the identification of “deal-critical” red flags is of far greater importance than the exhaustive listing of all legal issues.

Mục lục bài viết

1. Change-of-Control Provisions. A Structural Risk Often Underestimated

One of the most significant, yet frequently underestimated, risks in M&A transactions is the existence of change-of-control provisions in key contracts.

Material agreements, including major customer contracts, financing arrangements, and distribution agreements, often require counterparty consent upon a change in ownership or control.

From a legal standpoint, such provisions are not defects. However, from a transaction perspective, they may pose a fundamental risk. If not properly addressed, the buyer may successfully complete the acquisition, yet lose critical contractual relationships immediately thereafter.

The consequence is not merely legal exposure, but a direct impairment of the economic value of the transaction.

2. Customer and Supplier Concentration. The Intersection of Legal and Commercial Risk

Legal due diligence does not operate in isolation from commercial realities. In many cases, legal risks become material only when assessed within the operational context of the target.

Where revenue is heavily dependent on a limited number of customers, or operations rely on a single or limited group of suppliers, the associated contractual arrangements become critical.

While such concentration may not constitute a legal breach, it may give rise to transaction-level risk, particularly where contracts include termination rights, renegotiation triggers, or change-of-control provisions.

In such circumstances, legal due diligence must extend beyond contract review to assess the stability and continuity of commercial relationships post-closing.

3. Disputes and Investigations. Impact Beyond Monetary Exposure

A common analytical error is to assess disputes based solely on their financial value. In practice, the significance of a dispute lies in its strategic and operational impact, rather than its monetary size.

Particular attention should be given to disputes involving core assets, those capable of setting legal precedent, or matters involving regulatory or governmental authorities.

Even low-value claims may carry substantial risk if they affect the target’s operational continuity, licensing status, or market reputation.

Accordingly, disputes must be evaluated through the lens of transaction impact, rather than purely financial metrics.

Legal Due Diligence – Red Flags That May Disrupt or Derail M&A Transactions

4. Hidden Employment Liabilities. Latent but Recurring Exposure

Employment-related risks are among the most common sources of hidden liabilities in M&A transactions.

Issues such as the misclassification of employees and independent contractors, non-compliance with social insurance or tax obligations, and inadequate internal policies may not be fully disclosed or readily identifiable through document review.

These risks tend to accumulate over time and often crystallize only after closing, resulting in significant financial exposure.

From a due diligence perspective, this requires a deeper analytical approach that goes beyond formal documentation and considers actual operational practices.

5. Accumulated Tax Risks. Deferred but Significant Exposure

Tax risks are inherently latent and often materialize only upon subsequent review or audit by tax authorities.

Unclear tax structuring, related-party transactions, and aggressive revenue recognition practices may not give rise to immediate issues, but may result in substantial liabilities in future tax assessments.

Accordingly, tax due diligence must incorporate not only current compliance, but also the risk of future reassessment and enforcement.

6. Ownership and Title. A Foundational Transaction Issue

A fundamental principle in M&A is that the seller can only transfer what it validly owns.

In practice, however, ownership of key assets such as intellectual property, land use rights, and regulatory licenses is not always clearly established.

Deficiencies in registration, transfer history, or legal entitlement may not be immediately apparent from formal documentation.

These issues are foundational in nature. Any uncertainty regarding ownership or title may directly affect the validity, enforceability, and value of the transaction

7. A Structured Approach to Risk Classification

At HTH and Partners, we do not limit our analysis to the identification of risks. We focus on categorizing risks based on their impact on the transaction.

Risks are typically classified into three categories.

First, risks that may prevent or materially delay the transaction. These must be resolved prior to signing or closing.

Second, risks that affect transaction value or structure. These are addressed through pricing adjustments, indemnity protections, or other contractual mechanisms.

Third, risks that can be managed or mitigated post-closing through operational or legal measures.

This structured approach enables a direct linkage between due diligence findings and negotiation strategy, as well as transaction documentation.

Conclusion

Legal due diligence is not an exercise in identifying every possible legal issue, nor is it the production of extensive reports.

It is a process aimed at identifying material risks, assessing their impact on the transaction, and enabling informed decision-making.

In this context, the true value of legal due diligence lies not in completeness, but in the ability to identify and address the risks that have the potential to disrupt, alter, or ultimately derail the transaction.

Disclaimer:

This article is intended for informational purposes only and does not constitute legal advice from HTH & Partners. The content represents the views of HTH & Partners and is subject to change without prior notice.

The legal provisions referenced in this article were valid at the time of publication but may have been amended or repealed by the time of reading. We strongly recommend consulting a qualified legal professional before applying any information contained herein.