One of the most persistent misconceptions in M&A practice is the assumption that a broader due diligence scope necessarily results in a safer transaction.

In reality, an unfocused and overly expansive scope may undermine, rather than enhance, the effectiveness of the due diligence process. Transactions do not fail because insufficient information is reviewed. They fail because the wrong information is prioritized, and the right risks are not properly identified or assessed.

At HTH and Partners, our experience consistently demonstrates that the quality of due diligence is not determined by the extent of review, but by the precision with which the scope is defined.

Mục lục bài viết

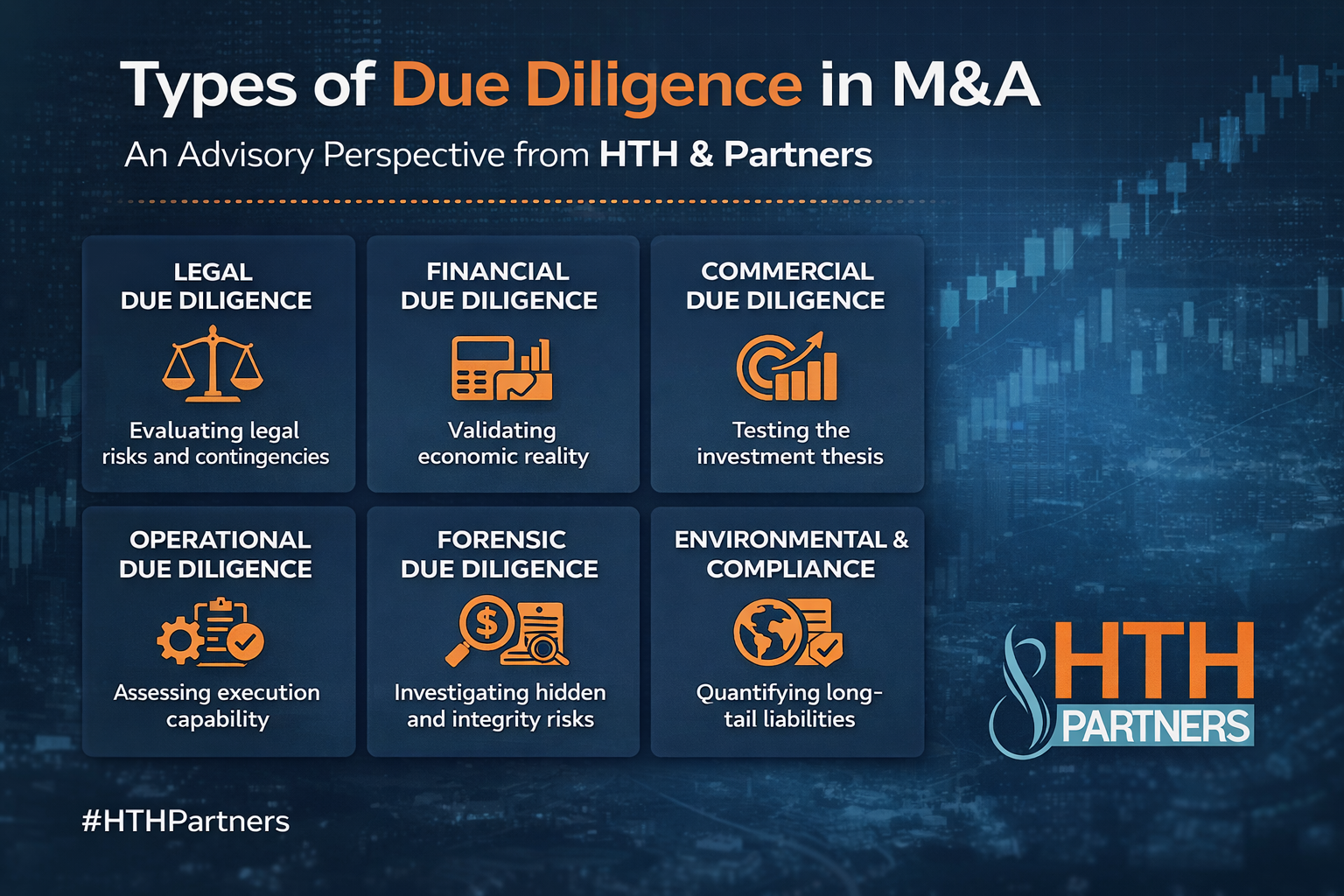

1. Scope as a Determinant of Decision Quality

The scope of due diligence does not merely affect efficiency. It directly shapes the quality of investment decision-making.

An overly broad scope typically results in:

- significant volumes of data with limited analytical hierarchy

- fragmented issue identification across multiple workstreams

- increased cost and extended transaction timelines

However, despite this apparent thoroughness, such an approach often fails to address the central question of the transaction.

Which risks have the potential to affect value, execution, or post-closing outcomes

Due diligence should therefore not be driven by what can be reviewed, but by what must be understood to support an informed investment decision.

2. The Absence of a Universal Scope

There is no standard or universally applicable due diligence scope.

Each transaction is defined by its own commercial, legal, and strategic context. Accordingly, the scope of due diligence must be calibrated based on a number of interrelated factors.

These include the nature and complexity of the target’s business, the size and structure of the transaction, the strategic objectives of the investor, the allocation of risk between the parties, and the level of reliance that can be placed on the seller’s disclosures and contractual protections.

A sponsor-led buyout, a strategic acquisition, and a distressed transaction differ fundamentally in their risk profiles. Applying a uniform due diligence approach across these transaction types inevitably results in inefficiencies and analytical blind spots.

3. Material Risk as the Core Organizing Principle

The definition of scope must be anchored in the identification of material risk.

Generic checklists, while useful as reference tools, often create a false sense of completeness. In practice, the most significant risks are highly context-specific and frequently concentrated in a limited number of areas.

For example, in technology transactions, intellectual property ownership and data protection compliance are often central. In manufacturing, environmental exposure and regulatory compliance may be determinative. In real estate transactions, title integrity, zoning restrictions, and land use rights are critical.

The primary risk in due diligence is not the failure to identify every issue, but the failure to identify the issue that is determinative to the transaction.

Common Misconception in Due Diligence – Broader Does Not Necessarily Mean Safer

4. Scope Discipline Under Transaction Constraints

Due diligence is inherently conducted under constraints. These constraints may arise from transaction timelines, cost considerations, competitive bidding dynamics, or limitations in access to information.

In this context, scope discipline becomes a critical component of transaction strategy.

At HTH and Partners, the scope of due diligence is aligned with clearly defined parameters, including materiality thresholds, applicable limitation periods, and areas of risk that are critical to the structure and viability of the transaction.

This disciplined approach ensures that resources are allocated efficiently and that the analysis remains focused on matters of substantive importance.

5. Scope as a Strategic Decision

Defining the scope of due diligence is not a technical or administrative step. It is a strategic decision that shapes how due diligence integrates into the broader transaction process.

An effective scope reflects a clear understanding of value drivers, a structured assessment of downside risks, and a forward-looking view of negotiation dynamics.

In this sense, scope definition determines not only what is reviewed, but how due diligence findings are ultimately translated into transaction terms, including pricing adjustments, representations and warranties, indemnity protections, and conditions precedent.

Conclusion

An effective due diligence scope is not defined by its breadth or level of detail.

It is defined by its selectivity, its focus on material risk, and its alignment with the commercial and legal objectives of the transaction.

Due diligence is not an exercise in reviewing everything. It is a process of identifying what matters and allocating resources accordingly.

From the perspective of HTH and Partners, discipline in due diligence is not measured by the extent of review, but by the ability to determine what does not require review.

Disclaimer:

This article is intended for informational purposes only and does not constitute legal advice from HTH & Partners. The content represents the views of HTH & Partners and is subject to change without prior notice.

The legal provisions referenced in this article were valid at the time of publication but may have been amended or repealed by the time of reading. We strongly recommend consulting a qualified legal professional before applying any information contained herein.